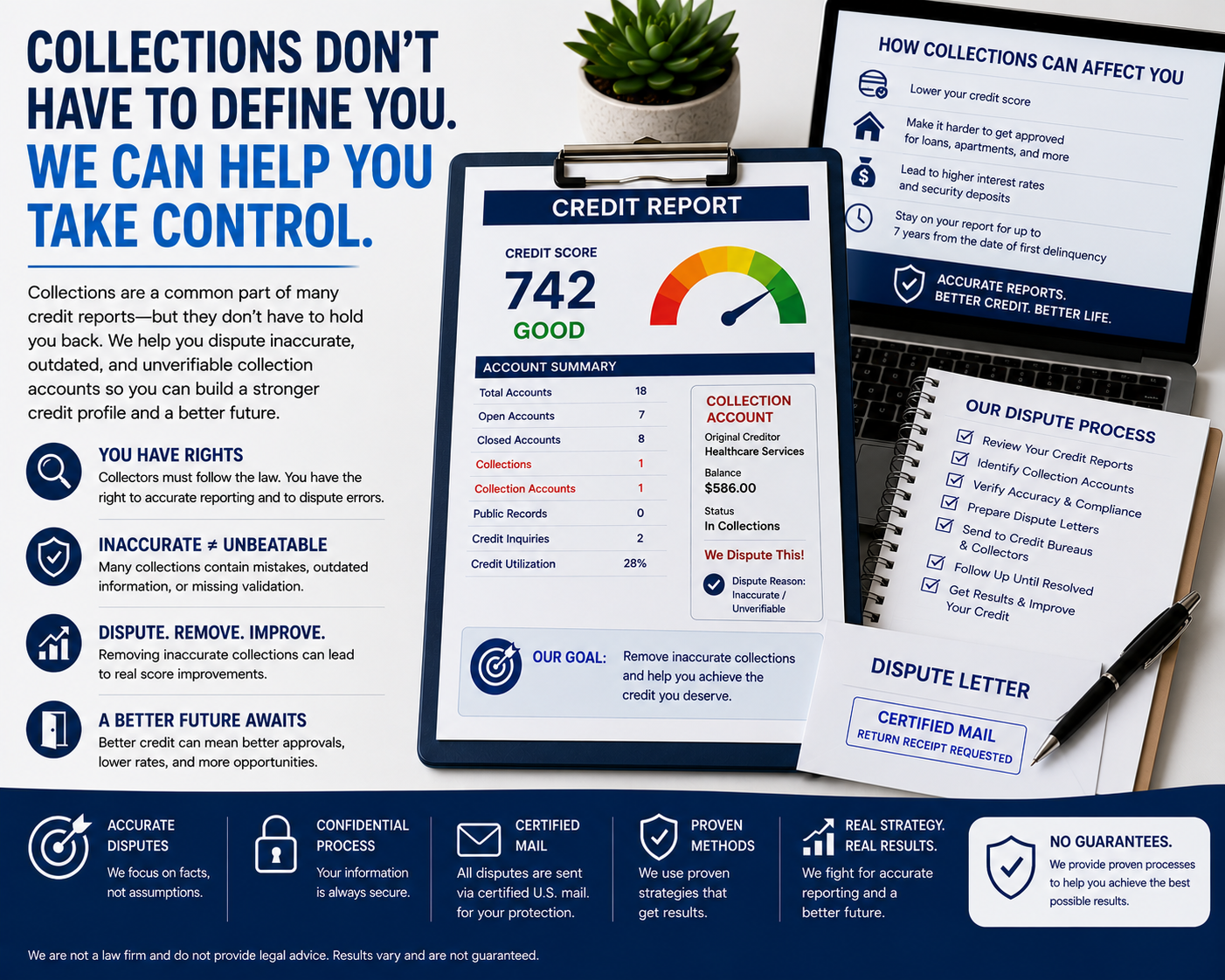

If you are looking for credit repair help in England, Arkansas, the goal is not to send random disputes or chase quick promises. The goal is to build a documented plan around credit report accuracy, score-factor improvement, and the timing needed for approvals such as a mortgage, auto loan, apartment, or better interest rate. Start with a simple consultation so your next step is based on your reports, your goal, and your timeline. Superior Credit Repair supports England, Arkansas clients through a statewide Arkansas service office signal. For appointment reference, directions, and consistent local trust information, use the Little Rock office location below. This Arkansas office reference helps keep the page geographically aligned while the credit repair plan remains specific to England and the consumer’s credit file, approval goal, and documentation timeline. Get directions to 400 West Capitol Ave, Suite 1700, Little Rock, AR 72201 Most people searching for credit repair near me in England, Arkansas are not dealing with one simple problem. They may have a collection account, late payments, high credit card balances, a charged-off account, a repossession, student loan confusion, medical bills, or personal information that does not match across all three bureaus. A strong plan separates those issues into two tracks: what needs to be reviewed for accuracy and what needs to be improved through better credit behavior. The first track is credit report accuracy. Every account should be checked for the correct balance, date, account status, payment history, ownership, creditor name, and bureau reporting pattern. If an item is inaccurate, incomplete, outdated, duplicated, or not properly verifiable, that gives you a reason to challenge the reporting. If the item is accurate, the better strategy may be rebuilding around it instead of wasting time on weak disputes. The second track is credit rebuilding. This is where many consumers in England, Arkansas make the fastest practical progress. Lower reported utilization, protect every due date, avoid unnecessary applications, and keep your accounts stable before a lender or landlord reviews your profile. Disputes can address reporting problems, but positive score factors help make your file stronger even while bureau investigations are pending. For a deeper foundation, review our guide on credit report errors. If collections are part of the problem, also compare your situation against the collections removal strategy. These internal resources support the same process used on this page: identify the facts, document the issue, and take the next step in the right order. When credit repair is tied to a home purchase, timing matters. Mortgage lenders usually look beyond the score alone. They review recent late payments, open collections, charge-offs, utilization, dispute comments, account age, new inquiries, and whether the file looks stable. A consumer in England, Arkansas who wants to prepare for FHA, VA, USDA, or conventional financing should avoid random disputes right before a loan review because unresolved disputes can create underwriting delays. The better approach is to build a runway. If you have 90 to 180 days before applying, review all three credit reports, lower revolving balances, collect documents for disputed accounts, and avoid new accounts unless they are part of a deliberate rebuild strategy. If the timeline is shorter, prioritize the items most likely to affect approval: recent lates, high utilization, active collections, charge-offs with inconsistent balances, and any identity data that makes the file look unstable. Many mortgage-focused files improve because utilization is handled correctly. Paying a card by the due date avoids late fees, but paying before the statement date can reduce the balance that reports to the bureaus. That reported balance is what scoring models evaluate. For consumers trying to buy a home in or near England, Arkansas, utilization planning may be the fastest controllable lever. Late payments require a different approach. Review whether the date, account status, and bureau reporting are consistent. If something is inaccurate, a targeted dispute may be appropriate. If the late payment is accurate, your plan may focus on building clean recent history and avoiding any new negative events. The late payment removal plan explains why late-payment strategy must be specific rather than generic. Pull reports from all three bureaus and compare every high-impact account. Look for mismatched balances, dates, statuses, creditor names, and payment histories. Make notes by bureau so the dispute strategy is targeted instead of repetitive. Not every item deserves the same attention. Recent late payments, open collections, high utilization, charge-offs, repossessions, and identity errors usually matter more than low-impact old items. Prioritization helps consumers in England, Arkansas avoid wasted effort. Keep creditor statements, payment confirmations, collection letters, settlement records, insurance explanations, identity documents, and prior bureau responses. Documentation makes follow-up stronger and helps you avoid sending vague disputes. Track bureau responses, update your priority list, lower utilization, protect current accounts, and plan the next round based on what actually changed. Credit repair is a sequence, not a one-letter event. An approval-ready credit profile is not perfect; it is understandable, stable, and supported by recent positive behavior. Lenders and landlords want to see that current accounts are paid on time, revolving balances are controlled, and negative items are either resolved, explained, aging, or being addressed through a legitimate accuracy process. If you are preparing for a mortgage, auto loan, apartment, business funding, or personal loan, avoid making your file look chaotic. Do not open unnecessary accounts, do not create fresh late payments, and do not send unsupported disputes that can trigger confusing results. Instead, build a quiet window where your reports become easier to approve. For England, Arkansas, that quiet window usually means checking reports monthly, keeping balances predictable, storing all credit documents in one place, and knowing which accounts are still waiting on bureau responses. The more organized you are, the easier it is to move from cleanup into approval preparation. Pricing and service expectations should also be clear. Before hiring any company, review what is included, how communication works, and what the provider does after bureau responses come back. Our credit repair pricing page can help you compare service expectations without relying on vague promises. The first mistake is disputing without a reason. A dispute should identify what is wrong, incomplete, outdated, duplicated, or not verifiable. If you dispute everything with the same wording, you make the process harder to track and easier to dismiss. The better method is specific, organized, and tied to the facts shown on the report. The second mistake is ignoring utilization. Many people in England, Arkansas focus on collections while their active credit cards report near the limit. That can keep scores suppressed even when negative items improve. Lowering reported balances is often one of the most controllable actions available. The third mistake is creating new damage during the repair process. One fresh late payment can hurt more than an old collection aging off in the background. Protecting current accounts is non-negotiable. Use reminders, automatic minimum payments, and a written monthly checklist so the rebuild side of the plan does not collapse. The fourth mistake is expecting one round to solve everything. Bureau responses vary. Some items are corrected, some are verified, some require additional documentation, and some may need a different follow-up strategy. A real credit repair plan adjusts based on the response instead of repeating the same letter. A good credit repair plan is easier to manage when your documents are organized before the first dispute is sent. Start with current copies of all three credit reports. Save screenshots or PDF copies of the accounts you want reviewed because reports can change while the process is underway. Keep creditor statements, payment records, collection letters, settlement confirmations, insurance explanations, identity documents, and proof of address in one folder so each account can be reviewed quickly. For consumers in England, Arkansas, documentation is especially important when accounts involve medical billing, debt buyers, student loans, repossessions, or old charge-offs. These accounts often include multiple parties and multiple dates. The bureau may show one balance, the creditor may show another, and a collector may use a different reference number. When you have organized records, you can challenge the exact reporting issue instead of relying on broad language. Documentation also helps you avoid duplicate work. After each bureau response, update a simple tracking sheet with the date sent, bureau, account name, dispute reason, result, and next step. If the response says the item was verified, compare what was verified against your records. If the bureau changes the balance or status, record that too. This creates a logical sequence instead of a pile of disconnected letters. A person preparing for a mortgage in England, Arkansas may need a different strategy than someone trying to qualify for an auto loan or apartment. Mortgage preparation usually requires more attention to dispute comments, recent late payments, utilization, and collections. Auto financing may focus more heavily on recent payment history, repossession reporting, and whether revolving balances make the file look overextended. Rental approval may depend on collections, judgments where applicable, identity consistency, and whether the applicant shows stable current accounts. This is why a local credit repair page should not push one generic answer for every file. The correct next step depends on the goal, the timeline, and the reporting pattern. If your goal is urgent, the plan should prioritize controllable factors first, especially utilization and current payment protection. If your goal is six months away, there is more room for documentation, follow-up disputes, and structured rebuild moves. If you are not sure where to start, begin with the account that creates the biggest approval problem and the action you can control fastest. For many people that means lowering a high revolving balance while reviewing collections or late payments for accuracy. For others, the first step is personal information cleanup because the bureau file itself contains mismatched identity data. A structured plan keeps the work tied to the outcome you actually need. After the first round is organized, keep the plan active. Review new bureau alerts, confirm payment dates, keep reported balances low, and save every response. Credit repair in England, Arkansas works best when each month has a purpose: one set of reporting issues to track, one rebuild habit to improve, and one approval goal to protect. Small monthly decisions often create the stability lenders want to see. Yes. Superior Credit Repair supports consumers looking for credit repair and credit restoration help in England, Arkansas. The process can begin with a consultation and a review of your goals, reports, and timeline. No. No legitimate credit repair company can guarantee specific deletions, approvals, score increases, or exact timelines. The focus should be accuracy, documentation, and consistent follow-through. Some files show early movement in 30 to 90 days, but complex profiles can take longer. Timing depends on the reporting issues, documentation, bureau responses, and the rebuild actions taken while disputes are pending. Protect every due date, lower revolving utilization, avoid unnecessary applications, keep documents organized, and track all bureau responses. Rebuilding while accuracy cleanup runs gives the file more ways to improve. They can be corrected or removed when the reporting is inaccurate, incomplete, outdated, duplicated, or not properly verifiable. Accurate negative information cannot be promised for deletion. Yes, credit repair services are legal when handled with proper disclosures, truthful claims, and no deceptive promises. Legitimate work focuses on credit report accuracy and consumer rights. Use this page as the local planning hub for England, Arkansas, then use the supporting guides that match the account type on your report. Helpful next reads include credit repair pricing, credit repair timeline, how to repair your credit, nationwide credit repair services, and credit report errors. Those pages give more detail on specific credit report problems while this page keeps the local plan organized around your approval goal. Important: outcomes vary by consumer file and bureau responses. Superior Credit Repair does not promise specific deletions, score increases, approvals, or timeframes. This page is general educational information and not legal advice.Credit Repair Help in England, Arkansas

Free Credit Review Request

Arkansas service office and local appointment signal

400 West Capitol Ave, Suite 1700

Little Rock, AR 72201

Credit repair strategy for England, Arkansas

Mortgage readiness and lender timing in England, Arkansas

A practical workflow you can follow

Step 1: Three-bureau review

Step 2: Prioritize by approval impact

Step 3: Document before disputing

Step 4: Rebuild while tracking

What approval-ready credit looks like in England, Arkansas

Mistakes that slow down credit repair

Documentation checklist for England, Arkansas

Different goals require different credit repair priorities

Monthly maintenance after the first review

Frequently asked questions about credit repair in England, Arkansas

Do you serve England, Arkansas?

Can you guarantee deletions or score increases?

How long does credit repair usually take?

What should I do while disputes are pending?

Can collections or charge-offs be removed?

Is credit repair legal?

Supporting guides for the next step